Britain’s current impasse goes well beyond Keir Starmer’s fragile position against a rising right-wing challenge. Beneath the Westminster drama is a deeper structural problem: elevated borrowing costs are not just a reaction to political instability but a judgment on the long-term sustainability of the UK’s fundamental economic model. Amid weak growth, low productivity, and mounting fiscal pressures, markets are pricing in more of the same.

The yield on a 10-year gilt, the UK equivalent of a U.S. Treasury bond, has moved in tandem with Britain’s political crisis. It has spiked when Starmer’s leadership came under pressure, eased when the political temperature fell. While the correlation is real, the interpretation it invites is wrong.

Yields on 10-year UK government bonds remain higher than those of every other G7 economy, a premium that predates Starmer, survived his Conservative predecessors, and will outlast whoever leads next. Britain’s elevated borrowing costs reflect a structural verdict on its economic model—not on any individual government.

Britain’s elevated borrowing costs reflect a structural verdict on its economic model—not on any individual government

A Premium Without Precedent

When the Middle East conflict drove a global bond sell-off in early 2026, the divergence between the UK and its peers became precisely quantifiable. The yield on 10-year German Bunds, Europe’s benchmark safe-haven bond, rose 42 basis points. French OATs rose 64 basis points. U.S. Treasuries rose 48 basis points. Gilt yields rose materially more, and among comparable economies only Australia carries a higher 10-year yield. The disproportion signals a distinct risk profile, consistently priced across multiple market episodes.

As of early June 2026, the 10-year gilt yield stood at approximately 4.95 percent, having eased from a peak of 5.13 percent—the highest since 2008—as political tensions subsided. The Bank of England’s base rate has been held at 3.75 percent since December 2025, following six successive cuts from the 2023-24 peak of 5.25 percent. Long-term gilt yields remain elevated despite that easing cycle because markets price not just current monetary policy but the UK’s medium-term fiscal and growth trajectory.

The Bank of England’s Dilemma

The Bank of England faces a genuine and worsening policy bind. Inflation eased to 2.8 percent in April 2026, down from 3.3 percent in March as energy base effects unwound. It remains materially above the 2 percent target, driven by energy price shocks from the Iran conflict. Yet options are limited. Cutting rates aggressively risks reigniting inflation; raising them risks deepening already weak growth.

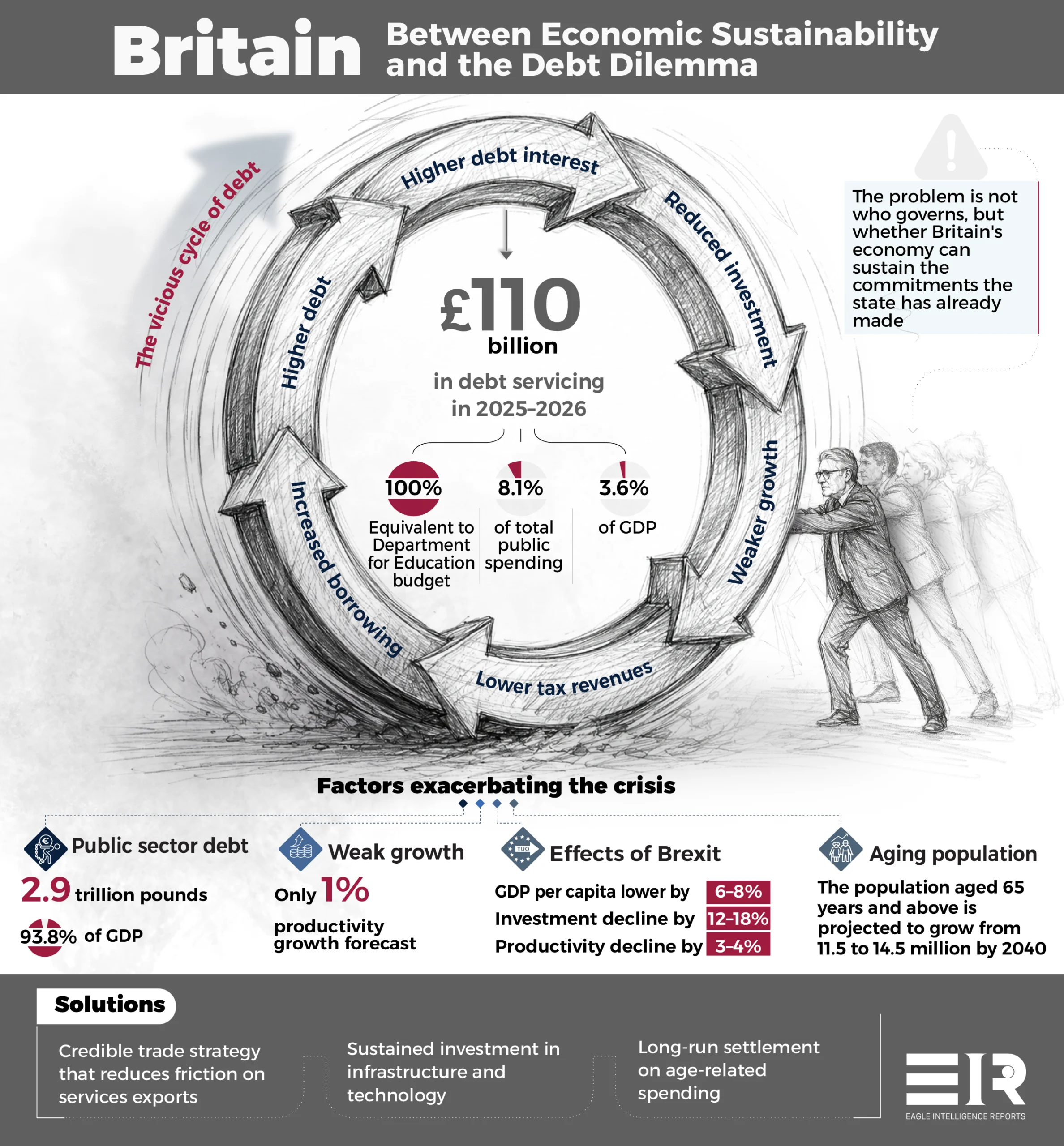

In a worst-case scenario in which oil prices are sustained above $130 a barrel, the Bank of England projects inflation peaking at 6.2 percent in early 2027. That could force the base rate back toward 5.25 percent within twelve months. Higher rates would push gilt yields further still and materially worsen debt servicing costs already running at £110 billion. Again, tightening deepens the recession risk while loosening validates market fears about inflation persistence. Neither path relieves the structural pressure on gilts.

Tightening deepens the recession risk while loosening validates market fears about inflation persistence. Neither path relieves the structural pressure on gilts

A further vulnerability compounds this. The UK holds the largest share of inflation-linked debt—known as index-linked gilts, or linkers—of any major developed economy, with approximately £620 billion outstanding. These instruments pay interest tied to the Retail Price Index, so when inflation rises, the government’s interest bill rises automatically. This explains why the 2022–23 inflation shock translated so rapidly into a near-tripling of annual debt interest costs, from £39 billion in 2019–20 to £110 billion in 2025-26. Markets accordingly treat UK inflation risk as a direct fiscal risk, not merely a monetary one.

The Debt Arithmetic

The fiscal position underlying those yields is severe by any measure. Public sector net debt stood at £2,911 billion at the end of March 2026, equivalent to 93.8 percent of GDP, up from 35 percent in 2007–08. The cost of servicing that debt, £110 billion in 2025-26, equals 3.6 percent of GDP and 8.1 percent of total public spending: among the highest levels in fifty years. The debt interest now roughly equals the entire Department for Education budget.

The government borrowed £129 billion in the financial year ending March 2026. In April 2026 borrowing was already running £3.4 billion above the OBR’s projection for that month. Debt as a share of GDP is projected to continue rising, settling at approximately 95 percent in the early 2030s.

Chancellor Rachel Reeves has responded with an unprecedented tax expansion. The overall burden is forecast to reach 38.5 percent of GDP by 2030–31, a post-1945 record. Measures include increases to employer National Insurance contributions and a multi-year freeze on income tax thresholds. The freeze pushes workers into higher brackets as wages rise, a mechanism known as fiscal drag. Further levies on dividends, property, and gambling complete the package. Fiscal headroom stands at £23.6 billion: nominally improved since November 2025, but historically narrow and calculated before the Middle East conflict escalated.

Taken together, these figures describe a government that has exhausted the conventional fiscal toolkit. It is borrowing at historic levels and taxing at post-war records without meaningfully stabilizing the underlying trajectory.

These figures describe a government that has exhausted the conventional fiscal toolkit. It is borrowing at historic levels and taxing at post-war records without meaningfully stabilizing the underlying trajectory

The Cost of Crowding Out

The annual debt interest bill directly displaces other public spending, a dynamic economists call crowding out. Each year, the government services existing debt before allocating a single pound to health, defense, welfare, or capital investment.

Defense illustrates the bind most sharply. The government has committed to raising NATO-qualified defense spending from 2.4 percent of GDP today to 2.5 percent by 2027, and to 3.5 percent by 2035. The OBR estimates it must spend approximately £6 billion more per year beyond current plans simply to keep defense on a linear path to that target. That increment competes directly with rising debt interest for a finite pool of resources. The Treasury has already conditioned the longer-term ambition on whether economic and fiscal conditions allow.

Welfare faces the same arithmetic from the opposite direction. Social benefits rose by £2.7 billion in April 2026 alone, driven by inflation-linked increases in state pension and Universal Credit—automatic uplifts that occur regardless of fiscal conditions. Governments historically defer capital budgets first when current spending overshoots. The pattern is visible in Britain’s infrastructure record across the past decade: productive investment sacrificed to protect current obligations.

The dynamic is self-reinforcing. Higher debt interest reduces fiscal space for growth-enabling investment. Lower growth reduces future tax revenues, which increases borrowing requirements, which—at elevated yields—adds further to the interest bill. The specific mechanism that makes this loop hard to break is the primary deficit: the UK borrows more than it spends on services before interest is counted. The OBR estimates the debt-stabilizing primary surplus at 1.3 percent of GDP; the UK ran a primary deficit of 2.2 percent of GDP in 2024-25. Without closing that gap, the debt stock compounds regardless of policy or personnel choices at the margin.

The Productivity Trap

The OBR’s March 2026 forecast assumes medium-term productivity growth of 1 percent annually, modest by historical standards and contingent on improvements the UK has repeatedly failed to deliver. Several structural forces explain that ceiling. Brexit is the most quantifiable. Research drawing on nearly a decade of post-referendum data estimated that by 2025, UK GDP per capita was 6-8 percent lower than it would otherwise have been. Investment was 12-18 percent lower, employment 3-4 percent lower, and productivity 3-4 percent lower. These losses accumulated gradually as trade barriers rose and firms redirected capital away from productive international activity. The OBR itself embeds a long-run productivity loss of 4 percent relative to EU membership as a baseline assumption.

What matters is the coverage of the Trade and Cooperation Agreement (TCA). The TCA governs goods trade with reasonable effectiveness. It provides no financial services equivalence and minimal coverage for the professional, legal, and creative sectors that drive UK export growth. These sectors face structural access barriers to their largest adjacent market, with no remedy inside the current political settlement on either side of the Channel. That constraint suppresses both investment incentives and productivity over the medium term. For a sovereign whose debt markets already price in structural weakness, a productivity ceiling with no near-term remedy compounds the financing problem at its root.

For a sovereign whose debt markets already price in structural weakness, a productivity ceiling with no near-term remedy compounds the financing problem at its root

The Demographic Constraint

The productivity problem is compounded by a demographic trajectory the state has not credibly priced into its long-run plans. England’s population aged 65 and over is projected to grow from 11.5 million to 14.5 million between 2024–25 and 2040. From mid-2026, deaths are projected to outnumber births, with a gap of approximately 450,000 by 2034. The old-age dependency ratio—the number of retirees relative to working-age adults—rises throughout the next two decades, compressing tax receipts while expanding age-related spending automatically.

The quantified fiscal pressure is substantial. Under current policy, state pension, pension credit, and winter fuel payments are projected to rise by 1.2 percent of national income by 2050, or £32 billion per year in today’s terms. Health and social care pressures are larger still: projected to rise by 4.1 percent of national income, approximately £105 billion per year in today’s terms, over the same period. These figures are the mechanical consequence of an aging population encountering a health system under above-inflation cost pressure. Medical technology, wage growth, and rising chronic disease prevalence drive that pressure—not political choice.

No government has produced a credible long-run strategy that confronts this combination. The triple lock on state pensions—guaranteeing annual increases by the highest of price inflation, earnings growth, or 2.5 percent—remains politically untouchable despite its compounding fiscal cost. Welfare reform proceeds under sustained resistance. The gap between what the state has committed to deliver and what the economy can finance is not narrowing. The figures imply that even holding all other spending flat, Britain faces a structural fiscal expansion driven by demography alone that no tax base growing at current rates can absorb.

The figures imply that even holding all other spending flat, Britain faces a structural fiscal expansion driven by demography alone that no tax base growing at current rates can absorb

What Markets Are Pricing

The gilt premium over German Bunds and French OATs encodes this accumulated assessment. Germany carries the institutional credibility of a constitutional debt brake and a manufacturing export base with deep global integration. France faces significant fiscal pressures of its own but sits within eurozone architecture that provides capital market depth and access to the European Central Bank’s Outright Monetary Transactions facility. That mechanism ended the eurozone sovereign debt crisis in 2012 by offering conditional backstop purchases of member state bonds. The Bank of England commands no equivalent. Deploying asset purchases to suppress gilt yields in an inflationary environment would aggravate the very problem it is already struggling to contain. The UK’s institutional buffers against fiscal stress are materially thinner than those of its European peers.

Goldman Sachs argued in early 2026 that gilts are penalized excessively relative to UK fundamentals, likely reflecting residual market memory of the 2022 mini-budget episode. There is a partial truth here: the Truss-Kwarteng episode, in which unfunded tax cuts triggered a gilt crisis requiring emergency Bank of England intervention, established a lasting political risk premium. What Goldman Sachs underweights is that this premium is not an exogenous distortion layered onto sound fundamentals but a symptom of the institutional thinness that made 2022 possible. The OBR’s independence and fiscal rules are self-imposed constraints—a government can loosen them at will, without the constitutional or supranational guardrails that anchor comparable sovereigns.

No Easy Exit

A change in leadership resolves nothing structural. Any successor government inherits the same productivity ceiling, the same debt stock, the same demographic arithmetic, and the same index-linked gilt sensitivity to inflation. A looser fiscal approach widens spreads and raises servicing costs. A tighter one compresses demand in an economy where private consumption is already constrained by elevated mortgage rates and limited real wage growth.

The exit requires durable productivity growth, sufficient to expand the tax base faster than the spending commitments it must finance. That requires, at minimum, a credible trade strategy that reduces friction on services exports, sustained capital investment in infrastructure and technology, and a long-run settlement on age-related spending. British politics has not yet been willing to negotiate that settlement transparently with the electorate. Each demands institutional patience and cross-party consistency the UK has rarely sustained.

If current trends persist, the choices narrow in ways British politics has not begun to confront openly. Debt servicing at current or higher rates will force explicit trade-offs between defense commitments, welfare entitlements, and public investment that incremental reform cannot avoid. A state that cannot finance its promises without sustained market tolerance will eventually face a market that withdraws it—as 2022 demonstrated briefly and incompletely.

Debt servicing at current or higher rates will force explicit trade-offs between defense commitments, welfare entitlements, and public investment that incremental reform cannot avoid

The adjustment, when it comes, will not be a political event but a fiscal one. It will be driven by the arithmetic of a primary deficit that compounds, a demographic bill that grows, and a productive base that has not expanded fast enough to service either. The longer the structural gap remains unaddressed, the fewer the options available to whoever is eventually required to close it.

The gilt yield measures the distance between Britain’s fiscal commitments and its productive capacity—and the market’s assessment of whether any government will close it. That distance, as of today, is wide and not narrowing.