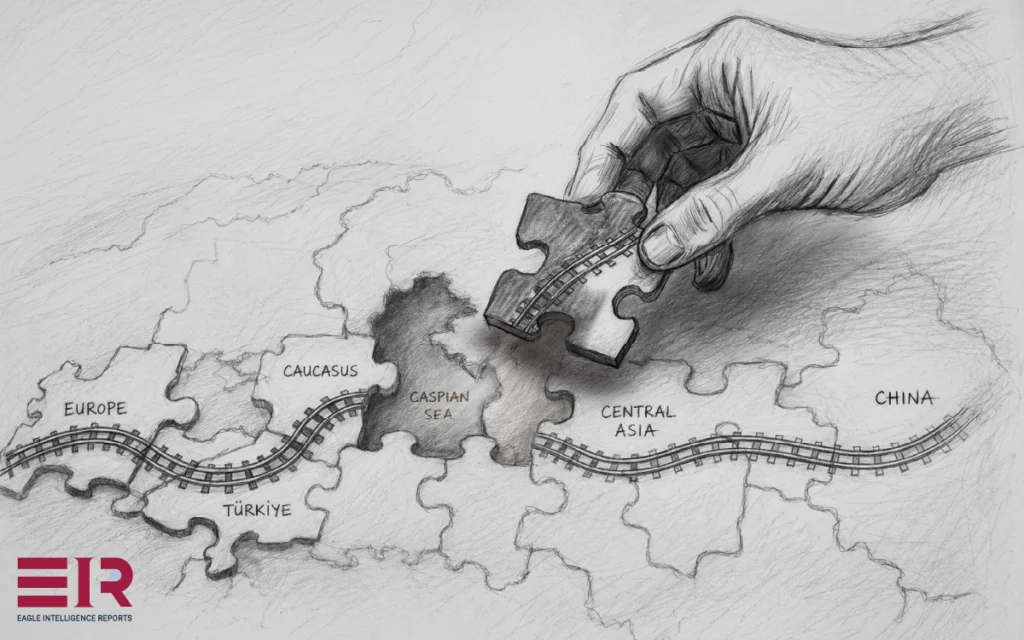

Eurasia is absorbing a series of strategic shocks. Russia is mired in its war in Ukraine. Israel and the United States have fought a war with Iran. A decades-long Armenia–Azerbaijan conflict has ended, and a new confrontation between Afghanistan and Pakistan looms. While the great powers are distracted or absent, a set of smaller states has moved through the opening. Their instrument is an old ambition made real: a working overland route linking China to Europe across Central Asia and the Caucasus, ground that empires fought over and long kept closed. Planners call it the Middle Corridor.

The deeper significance is that, across Eurasia, the traditional land-power dominance is fading. Russia and Iran long shaped the continent by holding territory and controlling who crossed it. A more flexible order is now emerging, built on infrastructure, connectivity, and shifting economic alignments. Geoeconomic change is driving geopolitical and strategic consequences, and the Middle Corridor is the clearest sign of where it leads.

Russia and Iran long shaped the continent by holding territory and controlling who crossed it. A more flexible order is now emerging, built on infrastructure, connectivity, and shifting economic alignments

No great power built this corridor. It is fundamentally a regional and collaborative project. It is the work of middle and small states of Central Asia, along with Azerbaijan and Turkey. They laid the track, bought the ferries, and modernized their borders to secure a route beyond the reach of any single great power.

Yet China is the indispensable partner. Its economy supplies the freight that fills the trains. Much of the capital and industrial capacity that went into financing and building the ports and railways came from China’s state-owned banks and construction firms. But while the project gives Beijing a faster path to Europe, the corridor answers first to the region that built it.

When sanctions closed the route through Russia and Houthi attacks closed the Red Sea, the world’s shippers turned to the one corridor through the middle that avoided both. The consequences are already visible. A single economic space is taking shape from Central Asia through the Caucasus to the Mediterranean. The states along it have won room to maneuver they rarely held before, diversifying their partners and dealing with great powers from firmer ground.

Washington and Brussels are moving into a region that others long treated as their own, as the advantages that underwrote Russian and Iranian influence quietly erode. The corridor is still young and far from finished. Yet it has already begun to loosen a grip that Moscow and Tehran held for centuries.

The Rise of the Middle Corridor

That shift did not happen on its own. The corridor’s rise owes much to the geostrategic conflicts occurring in Eurasia and the end of hostilities between Armenia and Azerbaijan. China has risen to a powerful, arguably primary, position in the global economy, and India’s economic profile is rising. Russia has failed to convert its extractive economy into a competitive industrial and high-tech one. These events have allowed the Middle Corridor to assume a pole position as a vehicle for transcontinental trade, transport, and connectivity at the expense of rival, competing projects. The corridor is one of many projects linking Europe and Asia. Its success, however, stems above all from the economic and political transformation of Central Asia and the Caucasus.

First, large-scale Chinese investment under Beijing’s Belt and Road Initiative (BRI) drove the construction of the necessary infrastructure. It also created a demand pull, bringing Chinese and Asian goods to European and Eurasian markets. Chinese demand and capital remain the corridor’s anchor. Without China’s sustained commodity flows, the route could not reach the scale needed to remain financially viable. Beijing also holds equity in the corridor itself through investments across Georgia, Azerbaijan, and Kazakhstan, all under the Belt and Road framework.

Chinese demand and capital remain the corridor’s anchor. Without China’s sustained commodity flows, the route could not reach the scale needed to remain financially viable

Second, the five Central Asian states have begun to cohere, especially after the 2016 change of leadership in Uzbekistan. Together with Azerbaijan, they showed a new determination to avoid conflict among themselves. Uzbekistan’s role was crucial, given its central regional position and astride the routes running west. Under President Mirziyoyev, it reversed Islam Karimov’s autarchic economic policies and fully embraced the logic of regional partnership and international economic integration. This cooperation, and a desire to curb terrorism through economic ties, pushed other states to act. Kazakhstan in particular took the lead in reconnecting Afghanistan to its neighbors and the wider world. The aim was to open lasting trade routes through it to South and East Asia.

The end of hostilities between Armenia and Azerbaijan followed. In 2025, the agreement on the Trump Route for International Peace and Prosperity across the disputed Zangezur region improved prospects for trade from China to Turkey and Europe. Simultaneously, the strong U.S. interest and presence in the Caucasus is finding its analogue in a concurrent expansion of Western investment throughout Central Asia. These processes both require a functioning corridor from Central Asia and the Caucasus to European and Mediterranean ports. Admittedly, the potential Pakistan-Afghan strife raises a possible cloud over this corridor’s prospects.

However, that danger helps explain why Central Asian states are making determined efforts to prevent conflict and expand trade through Afghanistan to Pakistan, India, and beyond. Apart from these trends, Russia and Iran’s policy failures and subjection to sanctions stopped corridors that traverse their countries from moving forward, reducing their ability to compete with the Middle Corridor. These sanctions stem from Russia’s war with Ukraine and the U.S.–Israeli war with Iran. But they are by no means the sole nor even the primary reasons for the failures of the alternatives to the Middle Corridor to take root.

Russia and Iran’s policy failures and subjection to sanctions stopped corridors that traverse their countries from moving forward, reducing their ability to compete with the Middle Corridor

Why the Alternatives Failed

Since the end of the Cold War, the search for trade corridors between Asia and Europe has been constant. A globalizing economy demanded them. Equally importantly, the new governments of the Caucasus and Central Asia sought new modes of connection to the world to prevent excessive dependence on Moscow and later Beijing. Meanwhile, Western governments, including the United States, searched for ways to access regional energy assets. At the same time, Russia sought to build on the Soviet experience of an integrated economy—particularly regarding energy—to bind the new states to it in a patron-client relationship. China sought lasting ties with the new states as well. Its first aim was to pacify its restless Muslim frontier in Xinjiang. It then sought export markets and political leverage abroad.

Out of the many proposals for new transcontinental arteries, three emerged as potentially viable corridors in the last decade. The Northern Corridor, which runs through Russia’s railways all the way to Europe and Baltic ports, is the straightest and simplest route. But even before sanctions, the poor quality of the railroad, maintenance issues, corruption, and underinvestment reduced its desirability as a trade route. And since sanctions have been imposed, its competitiveness has worsened. The decisive issues here are sanctions exposure, compliance risk, insurance and payment dangers, and the reputational and security risks of shipping through Russia. Those factors have materially reduced the corridor’s attractiveness for many European-facing supply chains.

The other alternative is the International North-South Transport Corridor (INSTC), which aims to connect Iran, Central Asia, and Russia through the Caspian Sea. INSTC could also bolster Indian trade with Central Asia, the Caucasus, and Europe, given Indian and Central Asian interest in utilizing Iran’s Indian Ocean port at Chabahar. Although in some segments of the project, cargo is moving, the impact of sanctions and war is felt, not to mention the political, insurance, reputational, and physical risks of the project. However, despite years of discussion of this project, neither Moscow nor Tehran invested enough resources or policy attention in it or in overcoming these obstacles to create a viable alternative to the Middle Corridor.

INSTC’s competitor, the India–Middle East–Europe Economic Corridor (IMEC), meant to establish a corridor from India through Hormuz, Saudi Arabia, Jordan, and Israel, remains essentially a concept on paper. The corridor was halted after the Israel–Gaza war, and the wider war in the Middle East means that it is not a viable practical alternative, much to India’s dismay. Likewise, maritime alternatives have failed to pick up the slack—and not only IMEC. The Houthi threat in the Red Sea has driven up shipping, insurance, and freight costs. Much traffic has diverted around Africa, cutting oil flows through Bab el-Mandeb and hitting Egypt’s Suez Canal revenues hard. Its revenue fell from about $10.3 billion in 2023 to under $4 billion in 2024 as shippers rerouted around Africa.

Energy Raises the Stakes

Houthi attacks from late 2023 cut energy flows through the Bab el-Mandeb Strait from about 8.7 million barrels per day in 2023 to roughly 4 million in 2024, a fall of more than half. Not surprisingly, this led Gulf energy producers to develop other pipelines and meet increased demand for Azeri and Caspian Basin oil and gas. This search for routes that bypass Iran runs through the region’s wartime moves. Talk of new pipelines could make Turkey a far larger energy hub, quite apart from its recent gas finds off the Black Sea coast. Should Central Asian and Azeri energy converge on Turkey, its weight in the global economy would rise sharply. The same flows would bind Central Asia, the Caucasus, and the Middle East into one system.

Talk of new pipelines could make Turkey a far larger energy hub, quite apart from its recent gas finds off the Black Sea coast

In the Gulf, the most clearly utilized pipelines are the Saudi crude pipeline to Yanbu on the Red Sea and the UAE’s pipeline to the Sea of Oman coast. Both bypass Iranian and Houthi threats but also require large-scale investment to meet demand. Iraq is negotiating to route crude through Syria to Mediterranean ports. There is also renewed talk of a pipeline to Eilat and onward to Ashkelon, bypassing the Houthis and the southern Red Sea. Such a link would draw Israel, already close to Azerbaijan, into the regional economy.

Likewise, Turkey and Saudi Arabia aim to rebuild the Ottoman-era Hejaz railway and extend it to Oman to create an alternative global trade route to the Strait of Hormuz. If this project materializes, it could also become a link in the Middle Corridor’s overland trade to the Middle East. This project is framed as an operational answer to war-disrupted maritime routes. Reporting suggests it could cut cargo transit between the Gulf and Europe from over 30 days by sea lanes to less than two weeks by overland routes. And the geopolitical implications for Turkey are obvious. Thus, regional elites, spooked by the Gulf war, are envisioning new trade and energy routes that might further integrate the Middle East, China, the Caucasus, and Central Asia in viable trade, transport, digital, and energy networks that could also stretch to Europe.

Growth of the Middle Corridor

Russia’s invasion of Ukraine in 2022 transformed the corridor’s standing. A marginal Eurasian route became a strategic alternative to both the Russian Northern Corridor and the Red Sea and Suez sea lanes. Since 2020, cargo volume has risen roughly fivefold, from about 0.8 million tons to between 4 and 4.5 million in 2024. The corridor has thus moved from niche diversion capacity to a fixture of Eurasian supply-chain planning. Shippers value it above all for avoiding both sanctions on Russia and Houthi attacks in the Red Sea. Transit performance along the Middle Corridor has also improved sharply, which is just as important as tonnage. Kazakhstan reports that travel time from Xi’an in China to Georgia fell from 55 to 18 days. Other analyses report similar findings. This trend reflects improved management, infrastructure, and overall quality improvement, which in turn generates greater predictability and lower costs.

A marginal Eurasian route became a strategic alternative to both the Russian Northern Corridor and the Red Sea and Suez sea lanes

Moreover, the trend toward greater investment in this corridor that has facilitated these improvements is continuing. Kazakhstan plans to build more than 5,000 kilometers of new or modernized track over the next four years. By its own account, Kazakhstan has invested over $35 billion in transport and logistics infrastructure since 2010. A parallel process has also occurred in the Western segment of the Corridor. The Baku–Tbilisi–Kars railway has undergone modernization and annual freight capacity has quintupled from one million to five million tons. Because the line is one of the core links carrying the corridor beyond the Caspian bottleneck into Turkey and Europe, that added capacity is both economically and strategically important.

These increased investments are also part of a larger geoeconomic process of a broad investment cycle across Kazakhstan, Azerbaijan, Georgia, and Türkiye. Kazakh authorities are adding rail lines, vessels, terminals, and border digitalization, buying additional ships, and upgrading Aktau and Kuryk. Azerbaijan is deepening port and rail capacity. Turkey is moving to ease the Bosphorus rail bottleneck through the INRAIL project, with rail capacity across the strait projected to rise from about three million to as much as 50 million tons a year. Track, ships, and terminals are the visible half of the story. The less visible half is political.

The Window and Its Limits

The Middle Corridor is not only a trade route but also a barometer of power. It measures how far Eurasia has transformed from an order set by the states that hold territory into one set by states that build links. The winners are the countries in between. They are gaining development, capacity, regional cohesion, and, above all, greater freedom in foreign policy.

The Middle Corridor is not only a trade route but also a barometer of power. It measures how far Eurasia has transformed from an order set by the states that hold territory into one set by states that build links

Chinese and Turkish influence will grow, and the two may end up as rivals across the region. Turkey in particular could become a hub for transcontinental and Middle Eastern trade, an old ambition of its leaders. Yet American and European investment gives the smaller states room to resist subordination to any single power. The corridor’s growth over the next decade rests on steady investment, on stability across a tense neighborhood, and on Western patience.

The losers are Russia and Iran. Their flagship projects are stalled, and they lack the means to build alternatives. China, by contrast, is buying its way into the new structure even as Russia is shut out of it. The prize is real, and for the West, it is worth holding because it denies Moscow, Tehran, and Beijing the power to seal the region off. If the corridor’s backers hesitate, the map may yet settle to the liking of the powers it was meant to leave behind.