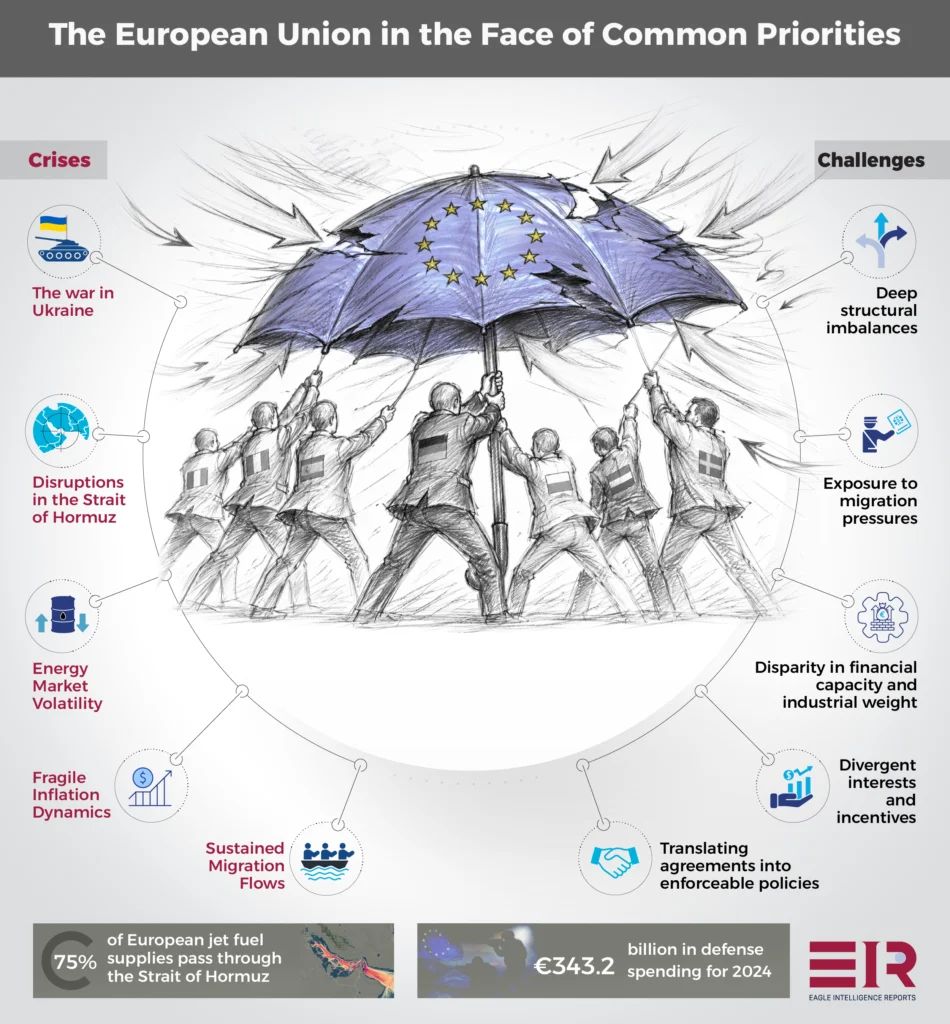

Europe is often described as fragmented, but that is only part of the story. The deeper problem is that several crises now converge within the same decision-making structures, forcing trade-offs and exposing the limits of EU’s capacity to translate shared priorities into coordinated action. The union remains united in principle but divided in practice.

Russia’s war against Ukraine still dominates the EU’s security thinking. Yet that war now sits inside a wider field of pressure that includes ongoing turmoil around Iran and the Strait of Hormuz, a renewed burst of energy volatility, fragile inflation dynamics, deep fiscal strain, sustained migration pressures, and a political landscape that is shifting even in countries once treated as stable anchors. Such pressures are not compartmentalized; they interact, accumulate, and constrain policymaking within increasingly narrow margins.

Russia’s war against Ukraine still dominates the EU’s security thinking. Yet that war now sits inside a wider fields of pressures that are not compartmentalized; they interact, accumulate

In principle, the EU can act coherently when three conditions hold: First, member states must share a common assessment of the threat. Second, they must retain sufficient fiscal and political capacity to mobilize resources around that assessment. Third, they must have the institutional capacity to translate agreement into implementation quickly and at scale. At present, all three conditions are under pressure.

The union still has a broad consensus that Russia poses the central military threat. It still has a working commitment to support Ukraine and strengthen its own deterrence posture. Yet the costs of action are no longer evenly distributed. They are increasingly spread across the union in ways that sharpen national differences rather than soften them. That is the core of its problem.

Russia as Strategic Baseline

The EU’s tension with Russia remains the baseline against which every other decision is judged. The war in Ukraine has closed off any serious prospect of a return to a light-footprint security order. EU member states’ defense expenditure has risen sharply since the war began in 2022. European states now spend more, plan more, and treat readiness with greater urgency than at any point in the post-Cold War era.

Yet higher spending has not solved the underlying problem. In one sense, Russia has made the EU more united by generating a shared recognition that deterrence can no longer be outsourced to the Americans at low cost. In another sense, it has exposed how uneven the capacity of member states to translate that recognition into capability remains. A wide gap lies between acknowledgment and implementation.

Here, geography continues to shape how that gap manifests. Poland and the Baltic states see urgency through the lens of direct exposure. Southern member states remain more divided between eastern deterrence and instability to the south. Large western economies accept that there is a need for military strengthening, yet they continue to move at different speeds, constrained variously by fiscal pressures, defense-industrial limits, and domestic politics.

Rearmament Without Full Capacity

That gap between strategic intent and practical delivery is clearest in the EU’s defense-industrial base. Brussels has responded with an expanding vocabulary of readiness, joint procurement, and industrial mobilization. The White Paper for European Defense Readiness 2030 and the SAFE instrument are both designed to accelerate joint investment and increase production output. Yet official and parliamentary assessments still point to bottlenecks, fragmented demand, supply chain weaknesses, and limited collaborative procurement.

The old problem persists. EU states are trying to build a harder security order with an industrial base and procurement culture shaped by decades of peacetime habits. Money is now moving faster than actual capability.

That lag matters because time has become a strategic variable. The continent does not have the luxury of rebuilding deterrence in calm conditions but must do so while Ukraine remains at war and while doubts about long-term American reliability have become a structural feature of European planning. The lesson many Europeans drew from the first Trump presidency was that transatlantic strain could be managed. The second has undermined that assumption. EU states may still depend on the United States for deterrence, intelligence, and strategic lift, yet their reduced posture imposes immediate economic and political costs. This is the reality of the European security environment.

Time has become a strategic variable. Europe does not have the luxury of rebuilding deterrence in calm conditions but must do so while Ukraine remains at war and while doubts about long-term American reliability have become a structural feature

Hormuz and the Return of Energy Shock

The latest flashpoint around the Strait of Hormuz illustrates this asymmetry with unusual clarity. Following failed talks with Iran, President Donald Trump announced that the United States would impose a blockade in the strait starting April 14. Iran has threatened retaliation, leaving European governments once again exposed to the risk that a crisis in the Gulf could quickly become a crisis in Europe’s own economies.

The importance of Hormuz as an energy chokepoint is obvious. For Europe, however, the crucial point is less about physical interruption than about price transmission. It takes very little disruption—or even the credible threat of disruption—to drive up risk premiums, unsettle fuel markets, and revive inflation fears across the continent.

This is where the EU’s energy story since 2022 must be understood properly. Member states succeeded in reducing one structural vulnerability by cutting reliance on Russian pipeline gas. Despite the economic consequences, that was a significant strategic achievement. Yet diversification also created a different kind of exposure where Europe is now more reliant on globally traded energy, on LNG markets, and on maritime flows shaped by events far from its own shores. In other words, the EU reduced one strategic vulnerability only to create another.

Inflation as a Political Constraint

Inflation in Europe now functions as a political constraint as much as an economic one. The ECB’s March 2026 staff projections revised headline inflation sharply upward for the year, driven largely by energy costs. It seems conceivable that large and persistent energy shocks will have disproportionately strong effects and can spread well beyond the energy component itself. Once that happens, the issue is no longer confined to household bills; it will extend into wage bargaining, borrowing costs, budget choices, and electoral politics.

Governments are therefore forced into trade-offs. They must decide whether to cushion consumers, preserve fiscal credibility, or redirect scarce money toward defense and industrial support. In practice, they cannot fully pursue all three at once.

This is the point at which Europe’s crises begin to interact and increase pressure within the system. Energy volatility does not simply make EU states poorer. It also makes their common strategy harder. A government facing renewed price pressure and angry voters has less room to maintain support for Ukraine at previous levels, less appetite for ambitious but costly industrial subsidies, and less willingness to shoulder collective burdens that carry immediate political costs at home.

Shared strategic priorities remain formally intact. But the degree of implementation across the union varies. Domestic politics decides how far they can travel in practice. As a result, coherence weakens when a common external shock produces divergent political responses within member states.

Hungary After Orbán

Hungary’s election underscores both the promise and the limits of political change inside the union. Viktor Orbán’s defeat by Péter Magyar’s Tisza party removes the consistent veto player in the EU’s internal politics on Russia, Ukraine, and rule-of-law disputes.

That means the likely disappearance of a recurrent obstacle to sanctions renewals, Ukraine financing, and broader coordination with NATO partners. For Brussels, this is a genuine procedural gain. It will find Europe easier to govern with Orbán out of power. Yet it should not confuse fewer vetoes with real strategic unity. Orbán’s exit reduces friction, but it does not erase the conditions that produced him nor the structural divides that run through the union. Member states still vary widely in fiscal capacity, industrial heft, migration exposure, and tolerance for prolonged confrontation with Russia.

Nor will Hungary immediately become a fully aligned actor. The incoming government will inherit institutions deeply shaped by over 15 years of Fidesz rule. Despite Orbán’s status as a symbol of resistance, Europe’s coherence problem was never just one man in Budapest. It lies in the fact that national interests and incentives within a broader supranational union still diverge even when formal obstruction falls away. Hungary’s change therefore improves throughput, but it does not settle Europe’s larger argument with itself.

Despite Orbán’s status as a symbol of resistance, Europe’s coherence problem was never just one man. It lies in the fact that national interests and incentives within a supranational union still diverge

Germany as Europe’s Execution Problem

Then there is Germany, which is central to that larger argument. The union’s ability to act still depends disproportionately on whether Berlin can convert broad agreement into actionable policy. Friedrich Merz’s arrival in office raised expectations in many European capitals that a more assertive German government would bring greater clarity after years of strategic drift.

The record so far is more mixed. Merz has the political language for a harder Germany, but he governs within a system constrained by coalition bargaining, fiscal caution, industrial anxiety, and the continued rise of the far-right Alternative for Germany. Recent political setbacks for his Social Democratic partners have only intensified those pressures. Germany remains indispensable to EU action, yet it does not yet look fully capable of driving it.

However, Germany occupies a special place in the European system. France can provide strategic vocabulary. Poland can supply urgency. The Commission can frame instruments and enforce rules. Yet it is usually Germany that determines whether large-scale EU commitments can be financed, legitimized, and executed. When Germany hesitates, Europe slows. When Germany is fiscally constrained, the union’s larger ambitions tend to be trimmed to fit the lowest politically acceptable denominator. The EU’s problem is therefore not only about disagreement between member states but also about the reduced execution capacity of the one state whose choices have system-wide effects.

Migration and the Politics of Scarcity

Migration adds another layer of strain because it is one of the few issues that combines fiscal cost, administrative burden, and immediate electoral salience. At the end of December 2025, 4.35 million people fleeing Ukraine held temporary protection status in the EU, with Germany, Poland, and Czechia carrying particularly heavy shares. At the same time, the broader asylum system remains uneven, with a handful of states receiving most applications, while the Pact on Migration and Asylum continues its transition from legislation into implementation. This creates a familiar pattern in which governments endorse solidarity in principle while fighting over distribution in practice. The result is not policy paralysis but persistent intra-union friction.

Migration undermines the EU’s capacity to act by distorting the political space in which other strategic decisions are made. It does not block action, but it alters the trade-offs. Money spent on reception, housing, border infrastructure, and integration is money that cannot easily be spent elsewhere. More important, migration remains one of the fastest routes by which external instability enters domestic political competition.

Migration remains one of the fastest routes by which external instability enters domestic political competition

Under these conditions, governments under pressure from the political right become more risk-averse across the board. They are less willing to accept redistributive burden-sharing deals within the union, less willing to defend open-ended commitments abroad, and more likely to frame policy through the language of immediate national control. The issue is bigger than migration policy itself. It affects the whole climate in which EU cohesion must be built.

Industrial Policy and Internal Asymmetry

The same tension is visible in industrial policy. EU states have moved decisively toward a more interventionist economic strategy, whether through the Net-Zero Industry Act, the Clean Industrial Deal state aid framework, or the broader push to develop strategic sectors domestically. The external logic is compelling. The continent wants to reduce dependence on Chinese clean-tech supply chains, avoid excessive reliance on the United States, and rebuild a defense-industrial base capable of sustaining prolonged competition.

Yet the internal politics are more complex. Larger member states have more fiscal firepower and greater capacity to exploit flexible state aid rules. Smaller states, by contrast, face tighter constraints and worry that strategic autonomy for the EU can become strategic advantage for Europe’s largest economies.

This structural tension is another reason the EU finds it so difficult to speak with one voice. Every move toward strategic autonomy creates a fresh argument about internal fairness. The union wants to act more like a geopolitical bloc, yet it remains a single market with enduring sensitivities about subsidy races, unequal capacity, and competitive distortion. In security terms, the answer often looks obvious: Build more in the EU. Buy more in the EU. Coordinate more in the EU. Yet in political terms, those choices still produce winners, losers, and suspicion. Each time the union must choose between speed and internal balance, cohesion within Europe is weakened.

Resilient, But Less Coherent

What, then, is the union becoming under these pressures? The answer is not a continent in collapse. EU member states remain more resilient than many of their critics expected. The union has absorbed the shock of Russia’s war, kept support for Ukraine alive, increased defense spending sharply, reduced its dependence on Russian gas, and preserved a functioning center in Brussels even as nationalist forces remain potent.

Orbán’s defeat may ease some procedural constraints in the short term. Yet resilience should not be mistaken for strategic clarity; there is no easy path forward. The EU bloc retains the capacity to respond, but it does so more slowly, more unevenly, and with narrower margins for error.

The central fact of the EU’s current condition is that its crises no longer arrive one by one. They accumulate. They interact, leaking into one another. And they all pass through the same overburdened machinery of budgets, coalitions, institutions, regulation, and public opinion.

The central fact of the EU’s current condition is that its crises no longer arrive one by one. They accumulate. They interact, leaking into one another

The result is a steady erosion of coherence, which is now harder to produce and harder still to sustain. The union’s challenge in 2026 and beyond is therefore larger than any single dossier. It is whether the bloc can still convert shared exposure into shared strategy and sustained action before the next shock arrives. On that question, the answer—for now—remains unsettled.