For two decades, Berlin treated China less as a geopolitical problem than as an economic solution. German carmakers sold more vehicles in Shanghai and Shenzhen than in Stuttgart or Munich. Chemical giants poured billions into Chinese mega-complexes. Machinery firms supplied the tools for the world’s most spectacular manufacturing boom. Politicians wrapped this symbiosis in a comforting doctrine: Wandel durch Handel or “change through trade”. Integrating China into global markets, the story went, would make it richer, more predictable, and ultimately more liberal.

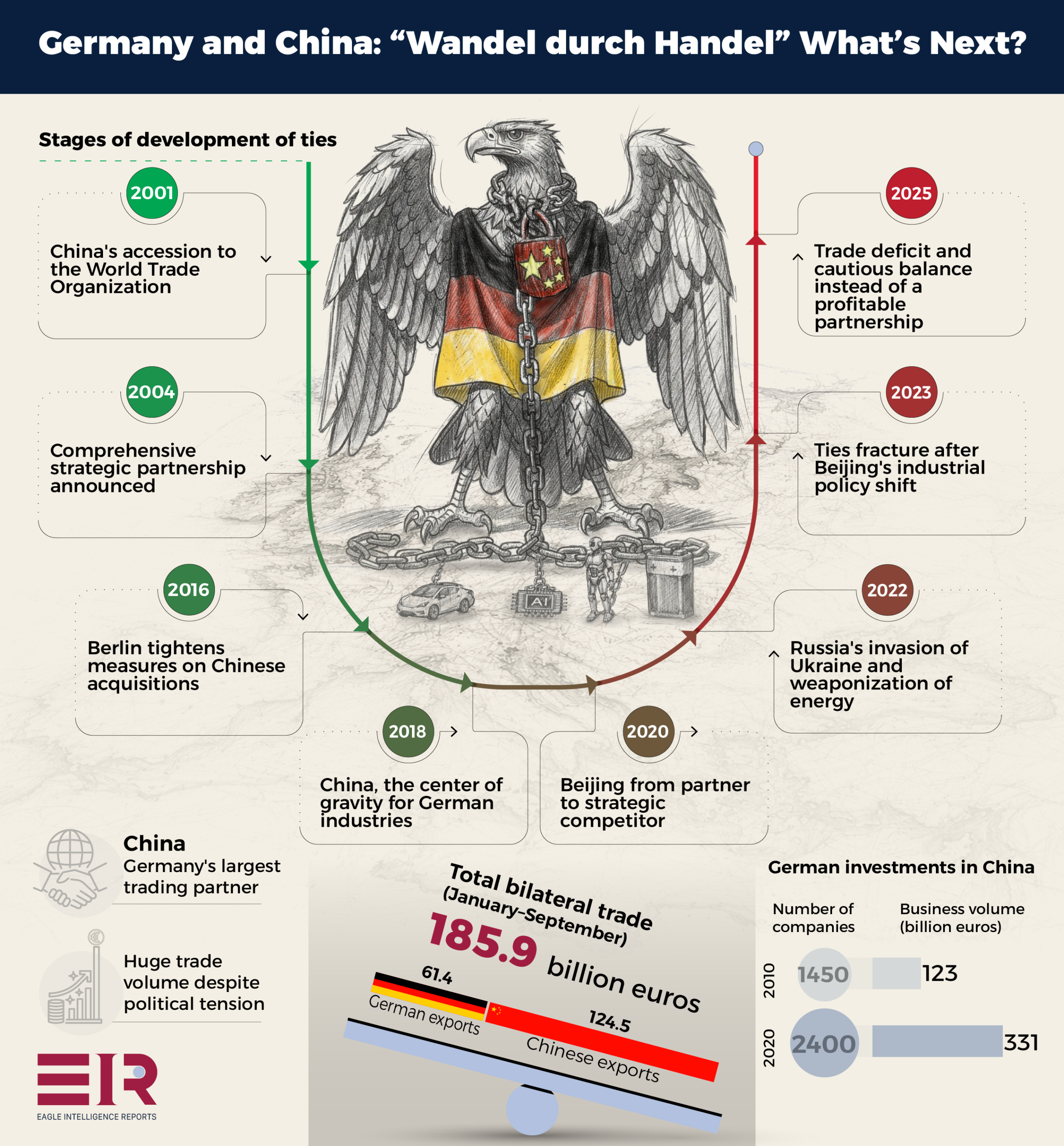

Today, no one in Berlin says that with a straight face. China is Germany’s most important trading partner, with foreign trade turnover of 185.9 billion euros from January to September 2025, and it remains a critical market for some of its most iconic firms. But the marriage of convenience that bound the world’s workshop to Europe’s industrial powerhouse is fraying. Beijing’s state-driven industrial policy has turned a lucrative customer into a ruthless rival. Its willingness to weaponize economic ties has made dependence look like vulnerability. Germany’s own shock over Russian gas — culminating in the Zeitenwende after the invasion of Ukraine — has forced a painful question: did it make the same mistake twice?

Germany is now trying to do something extraordinarily difficult: reduce its exposure to China without blowing up the relationship, to “de-risk,” not decouple. Whether that balance can hold will shape not only Europe’s economic future, but also the emerging geometry of great-power rivalry.

Germany is now trying to do something extraordinarily difficult: reduce its exposure to China without blowing up the relationship

A Comfortable Dependence

The modern relationship began with a simple, powerful complementarity. China needed machines, chemicals, and cars. Germany excelled at all three. After China’s entry into the World Trade Organization in 2001, trade between the two countries grew by several hundred percent. China became Germany’s single biggest goods trading partner. At a time when much of the West felt the sting of the China shock, German exporters enjoyed a China boom.

Politically, the relationship looked almost exemplary. In 2004, Berlin and Beijing announced a “strategic partnership,” upgraded a decade later to a “comprehensive strategic partnership.” Under Angela Merkel, intergovernmental consultations became routine. She traveled to China more than any other Western leader. When human rights or Tibet caused friction, these issues were treated as compartmentalized irritants, not structural problems.

Merkel embodied the aforementioned prevailing view: trade and investment could tame politics. By deeply integrating an authoritarian state into the rules-based trading system, Germany believed, it would gradually socialize China into that system’s norms. Economic interdependence was not only profitable but also supposed to be transformative.

German firms rushed in. Auto manufacturers built joint ventures and assembly plants. Machinery companies set up factories and service centers. Chemical giants announced multi-billion-euro investments along China’s coast. By the late 2010s, China had quietly become the center of gravity for Germany’s industrial establishment. A decade earlier, only around 1,450 German subsidiaries operated in the country; by 2020, that figure had climbed to nearly 2,400, according to data compiled by the Bertelsmann Stiftung. Their combined turnover more than doubled in the same period, rising from roughly €123 billion in 2010 to about €331 billion in 2020, a transformation so swift that it went largely unremarked in Berlin even as it reshaped the foundations of German industry.

Even then, the balance of risk was uneven. Germany depended on China as a growth market. China depended on Germany as a supplier and source of technology but deliberately worked to reduce that dependence over time. As long as the relationship felt like a win-win, few in Berlin wanted to look too closely at the asymmetry.

There were warnings. China’s overcapacity in steel, solar panels, and shipbuilding undercut European producers. Market access for foreign firms remained uneven. The 2016 takeover of German robot-maker Kuka by a Chinese appliance company rang alarm bells in the economics ministry and intelligence services. In response, it spurred tighter screening of strategic acquisitions.

But such episodes were treated as manageable glitches in an otherwise successful model. Even as the country’s main industry federation began talking about China as a systemic competitor, the chancellery still pushed for an ambitious EU–China investment agreement. It took a convergence of shocks to break that complacency.

From Partner to Systemic Rival

Three forces have driven Germany’s reassessment: First, China stopped playing the role Germany had assigned it. Under Xi, Beijing embraced an overtly nationalist, state-led development model. The Made in China 2025 plan laid out a strategy to dominate key high-tech sectors: robotics, aerospace, electric vehicles, artificial intelligence. These were precisely the domains where Germany had long excelled.

Backed by subsidies, procurement rules, and pressure on foreign firms to transfer know-how, these Chinese competitors rapidly caught up. In electric vehicles and batteries, they surged ahead. German carmakers that had once owned the Chinese market now faced domestic challengers producing cheaper, increasingly sophisticated EVs and exporting them to Europe. Telecoms, high-speed rail, renewable energy hardware: sector after sector saw similar patterns. China had transformed from a reliable outlet for high-value exports to a direct competitor, beginning to erode German firms’ market share at home, in China, and in third countries.

China had transformed from a reliable outlet for high-value exports to a direct competitor, beginning to erode German firms’ market share at home, in China, and in third countries

Second, China began demonstrating how easily interdependence could be turned into leverage. When Lithuania allowed Taiwan to open a representative office under the name Taiwan rather than Taipei, China quietly choked Lithuanian exports and blocked goods that contained Lithuanian components. As a result, European policymakers suddenly understood how a supply chain could be used as a weapon.

German officials also watched with increasing alarm as Beijing restricted key materials, such as gallium and germanium used in semiconductors, or hinted at future controls on rare earths. China dominates the refining of many minerals vital to the green transition that Germany is betting its economic future on. Each new export control or threat of one made the phrase economic security sound a little less abstract.

At the same time, Chinese state-owned companies were buying stakes in critical European infrastructure, including ports. In Germany, a contentious decision to allow a Chinese shipping giant a stake, albeit reduced, in a Hamburg terminal became a national controversy. Debates over Huawei’s role in 5G networks followed a similar trajectory: initial openness, mounting security concerns, and ultimately a belated move to exclude Chinese vendors from core infrastructure.

The cumulative effect was to shatter the idea that trade could be quarantined from geopolitics. Economic ties themselves had become part of the geopolitical battlefield.

Third, the value gap widened, and the Germans noticed. China’s mass detention of Uyghurs, the issue surrounding Hong Kong’s autonomy, and increasingly aggressive rhetoric and military maneuvers around Taiwan made it harder to treat political differences as background noise.

Germany’s previous coalition government promised a “values-based” foreign policy. Its coalition agreement mentioned Taiwan positively for the first time. The former foreign minister Annalena Baerbock (Greens) openly criticized China’s human rights record and labeled Xi a dictator.

The Russia Shock and the Birth of De-Risking

If Merkel’s China policy rested on an optimistic theory of change, it was also built on a practical assumption: that the economic benefits of interdependence outweighed the risks. That belief was shattered by Vladimir Putin. When Russia invaded Ukraine in 2022 and weaponized energy, Germany found itself scrambling to replace supplies and absorb a historic price shock.

The lesson for China policy was obvious and brutal. If Germany could be so grievously exposed to a middle-ranking petrostate, what did it mean to be similarly exposed to the world’s second-largest economy?

The response came in two linked concepts that now dominate European debates: economic security and de-risking. Unlike the American talk of “decoupling,” de-risking acknowledges that China will remain an indispensable player in the world economy. The goal is not to cut ties entirely, but to reduce excessive dependence while insulating critical sectors: advanced technology, defense-related inputs, key infrastructure, and strategic raw materials.

Germany’s first national security strategy and its first China strategy, both released in 2023, adopted this language. Together, they describe China simultaneously as partner, competitor, and systemic rival, but stress that competition and rivalry have become the dominant aspects of the relationship. They promise tighter export controls, more rigorous investment screening, and a reorientation of trade promotion instruments to discourage excessive exposure to any single country.

Practically, this has meant capping state guarantees for investments in China, signaling to firms that the government will no longer underwrite unlimited expansion there. It has also involved supporting EU-wide tools against economic coercion and backing infrastructure and raw-materials initiatives designed to reduce dependence on Chinese suppliers. Behind the jargon lies a clear shift: Germany is moving from cheerleading -style engagement to managing risk.

The New Imbalance and Pullback

The numbers are already showing just that. While China has, as mentioned before, taken over the US as Germany’s biggest trade partner again, the drama lies in the details. On one side, German imports from China surged to about €124.5 billion, driven by electrical goods, machinery, and components. On the other, German exports to China shrank sharply, down to around €61.4 billion, representing a 12 percent drop. Germany now runs a pronounced trade deficit with China, even as total trade remains immense.

Germany now runs a pronounced trade deficit with China, even as total trade remains immense

What once was a steadily rising engine of German exports, Chinese demand for German machinery, cars and industrial goods, has largely stalled. Growth has faded, regulatory headwinds have multiplied, and competition from Chinese domestic producers undercuts the old dynamic. At the same time, cheap Chinese imports continue flooding German shelves, from consumer electronics to capital-goods components, tilting the balance in a way that increasingly feels like de-industrialization.

For many German firms, especially in the small- and medium-size (Mittelstand) sector, the calculus has changed. Export hopes are dimmer, compliance burdens heavier, and the political risk of doing business with Beijing is harder to justify. Meanwhile, a handful of large corporate groups, the carmakers, the chemical giants, still treat China as a core market, reinvesting and defending their positions. But for the broader German economy, the old story of ever-closer integration is being replaced by a wary balance: trade with China remains vital, but the costs and strategic risks are growing.

Can a Transactional Relationship Work?

Economic logic still argues against a clean break. Germany cannot meet its climate goals without massive imports of solar panels, batteries, and critical minerals, sectors China dominates. China still benefits from German engineering, industrial software, and certain high-end machines. Tens of thousands of German jobs are tied to China business, and Chinese consumers still want German cars and luxury goods. So, what might a managed, transactional relationship look like?

Climate and green technology are the most obvious pillars. Both countries have long-term decarbonization targets. Germany needs cheap hardware, while China needs markets and technical expertise. German and Chinese engineers collaborate on hydrogen, grid management, and energy-efficiency technologies.

If Berlin, under the current Friedrich Merz government, is serious about de-risking, it will invest in alternative suppliers and domestic production. But for the foreseeable future, China will remain a dominant partner in many green supply chains. That reality creates an incentive to keep at least this part of the relationship stable, even when other areas are contentious.

Selective supply chain diversification offers another middle ground. Instead of trying to extract China from every link, German firms can reduce single-country dependence in critical nodes, while keeping China as one supplier among several in less sensitive areas. A carmaker might add factories in Mexico or Southeast Asia but still source some components from China. A chemical company might secure lithium from Australia while continuing to sell specialty chemicals into the Chinese market.

For China, too, economic pragmatism argues for avoiding needless confrontation. Western markets still matter. Being seen as an unreliable supplier risks accelerating precisely the decoupling Beijing wants to avoid.

Finally, there’s still room for ongoing diplomacy and compartmentalized cooperation. Germany and China still coordinate in multilateral forums on issues like climate finance, global health, and financial stability. Academic and cultural exchanges persist, though under greater scrutiny. City partnerships, student mobility, and business networks create constituencies on both sides invested in avoiding an outright break.

There’s still room for ongoing diplomacy and compartmentalized cooperation. Germany and China still coordinate in multilateral forums on issues like climate finance

This is a much more modest vision than the starry-eyed forecasts of a decade ago. It does not rely on the illusion that trade will liberalize China. It accepts rivalry and incompatibility in many domains, yet it tries to salvage a working relationship in those areas where interests still overlap. The question is whether this narrow path is politically sustainable.

The Gravity of Great-Power Rivalry

Several forces pull against the possibility of a stable, transactional relationship.

The first is ideology. The gap between a one-party, increasingly repressive China and Germany is not going to close. Every new crackdown, every hostage-taking or show trial aimed at foreigners or dual nationals, every escalation over Taiwan makes it harder for German leaders to justify engagement.

The second is the conflict between US–China rivalry and German strategic culture. Germany’s defense, to this day, depends on NATO, and its foreign policy continues to reflexively gravitate toward transatlantic consensus, if sometimes with a lag. As Washington and Beijing harden their confrontation, Berlin will face mounting pressure to align more explicitly with US positions on technology controls, sanctions, and security issues in the Indo-Pacific.

As Washington and Beijing harden their confrontation, Berlin will face mounting pressure to align more explicitly with US positions

Taiwan is the most explosive scenario. If China were to mount a military attack on the island and the United States responded with sanctions and export controls, would Germany really try to maintain business as usual with Beijing?

Even short of war, the tightening US regime of semiconductor and high-tech export controls will increasingly force German firms to choose between access to the Chinese market and access to American technology and finance. For most, the choice is obvious. For Berlin, each new restriction imposed jointly with Washington chips away at the space for a balanced, purely economic engagement with China.

The third is momentum. Decoupling is not a singular act but a process. Each investment that goes to the United States or India instead of China; each factory moved from the Pearl River Delta to Vietnam; each research partnership quietly canceled; each new security review that blocks a Chinese acquisition — these are one-way decisions.

Reversing them later would require more than goodwill; it would require convincing firms to undo costly restructuring and voters to accept renewed dependence on a state they have learned to distrust.

Beijing is pursuing its own version of de-risking: the dual circulation strategy that emphasizes domestic demand and homegrown innovation. Chinese policymakers speak openly about preparing for a hostile external environment. In practice, that means reducing reliance on Western technology and markets wherever possible. Germany’s attempt to reduce Chinese risk collides with China’s effort to reduce Western leverage.

Over time, two partially separate economic spheres could emerge: one centered on the United States and its allies, another around China and its partners. Germany, which once served as a bridge, will find it increasingly difficult to straddle the gap.

A Bellwether for the West

None of this will be cost-free. A serious reduction in economic ties with China will hit German growth, at a time when Europe’s biggest and most important economy already struggles. Export-oriented sectors will need time to find alternative markets. Diversifying supply chains and duplicating capacity is expensive. Consumers will pay more for goods once supplied cheaply from China. Climate policy may become more costly if Europe insists on localizing production rather than relying on Chinese scale.

Germany’s China debate is not just another chapter in the long saga of European angst about globalization, but a bellwether of something larger: how liberal democracies will navigate a world in which their main economic partners are also their main systemic rivals.

No Western country bet as heavily on the notion that commerce could transform China as Germany did. No major European economy is as deeply intertwined with Chinese industry as it is. If Berlin concludes that it cannot manage this dependence safely, others will take note.

No Western country bet as heavily on the notion that commerce could transform China as Germany did. No major European economy is as deeply intertwined with Chinese industry as it is

The likely outcome is not a dramatic divorce but a gradual, uneven uncoupling. This will involve a partial, messy, but real reordering of economic ties. Trade will continue, especially in non-strategic sectors. Some German companies will still make fortunes in China; some Chinese companies will still invest in Europe. Climate cooperation will remain both necessary and tempting.

But the age when Germany spoke of China as an indispensable partner, and treated political differences as background noise, appears over. The vocabulary has changed: from change through trade to systemic rivalry, economic security, and de-risking.

It signals the end of an era in which interdependence was assumed to be inherently stabilizing. Germany has discovered, belatedly and painfully, that in a world of authoritarian great powers, economic integration can amplify risks as well as distribute rewards.

Whether Berlin and Beijing can negotiate a new equilibrium, a cooler, more conditional, but still productive relationship, or slide toward a deeper rupture will depend on choices they have not yet made. It will hinge on how China acts toward its neighbors and its own citizens, how the United States manages its rivalry with Beijing, and how much economic pain German society is willing to bear in the name of security and values.