President Trump’s nomination of Kevin Warsh to chair the Federal Reserve places the central bank at a crucial juncture. Warsh’s sudden conversion from a diehard inflation hawk to an advocate of Trump’s interest rate cuts, combined with fiscal fragility, political pressure, and perilous macroeconomic conditions, creates a looming threat to the Federal Reserve’s cherished independence and, by extension, the credibility of the U.S. dollar.

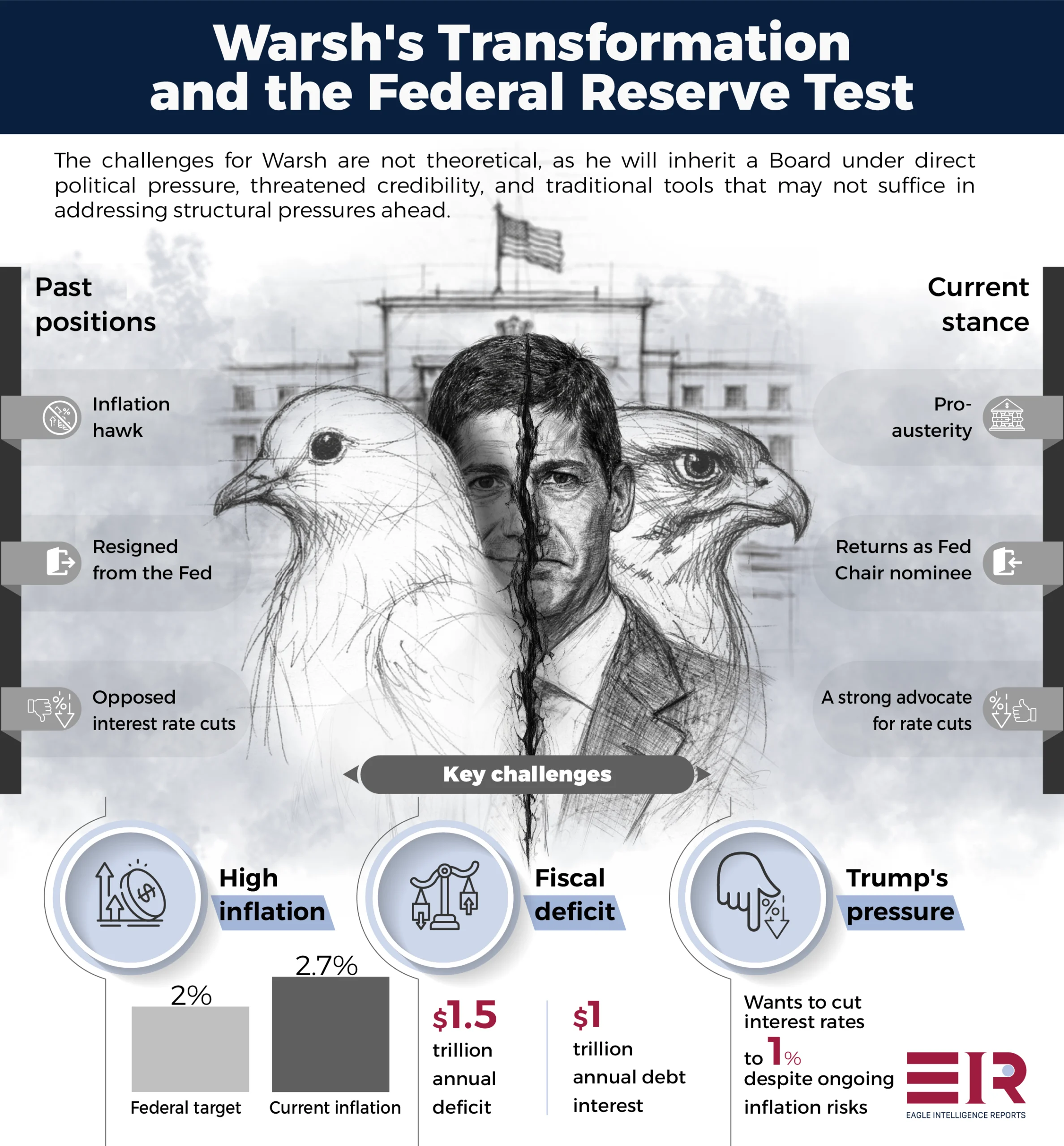

This nexus of risks occurs at what may be the most structurally dangerous moment for U.S. monetary policy since the era of Paul Volcker, the legendary cigar-chomping Fed chair who rescued the nation from raging inflation in the 1980s. The federal debt now exceeds 120 percent of GDP. Annual deficits surpass $1.5 trillion. Debt service costs exceed $1 trillion per year. The U.S. Treasury must roll over maturing securities at interest rates far higher than those that prevailed when they were issued. Inflation remains stubbornly above the Fed’s 2 percent target. And President Trump advocates future rate cuts that could drive prices higher.

The tension between fiscal expansion and monetary policy restraint creates a fragile balance where a misstep by an untested Fed chair could trigger bond market turmoil, threaten the dollar’s reserve status, and taint America’s global financial credibility.

A misstep by an untested Fed chair could trigger bond market turmoil, threaten the dollar’s reserve status, and taint America’s global financial credibility

Politics and Criminal Probe Haunt Nomination

Warsh, a conservative and former Fed governor, was nominated by President Trump to replace Jerome Powell, whose term as chair expires in May. In announcing the appointment, Trump avoided any explicit mention of Warsh’s shift in position on interest rates, but he later said in an interview that Warsh “certainly wants to cut rates.” Trump wants cuts quickly, too—perhaps down to as low as 1 percent—to curtail the cost of government borrowing and deliver lower short-term lending costs to voters ahead of the 2026 midterm elections, which are critical to the president’s hold on power.

The nomination also arrives amid an unprecedented Department of Justice criminal investigation of Powell. A DOJ subpoena, issued after Trump and Powell sparred publicly, states that the Fed chair is under investigation for alleged perjury during June 2025 congressional testimony regarding cost overruns for renovations to the Fed’s headquarters building. The probe, combined with Trump’s attempt to fire Lisa Cook, another Fed board member, has been widely interpreted as a thinly veiled attack on the Fed’s institutional independence.

Senator Thom Tillis, a North Carolina Republican who holds a swing seat on the Senate Banking Committee, has vowed not to advance the Warsh nomination until the investigation is “fully and transparently resolved.” Tillis, who is not running for re-election, says he will maintain his blockade until he vacates his Senate seat on January 3, 2027, leaving the nomination in limbo. Meanwhile, the Cook case is now pending before the U.S. Supreme Court.

Although his term as chair ends in May, Powell’s term as a governor with voting rights does not expire until January 31, 2028. Although most Fed chairs leave the board once their chairmanship ends, Powell could remain and become an influential voice in rate-setting votes. This possibility would complicate Warsh’s ability to build consensus on the Fed’s 12-member rate-setting committee. Powell has not disclosed his plans. Regardless, Warsh must contend with the legacy of a widely respected predecessor who brought inflation down from 9.1 percent in June 2022 to 2.7 percent without triggering a recession—all while frequently and publicly disagreeing with the president.

Warsh must contend with the legacy of a widely respected predecessor who brought inflation down from 9.1 percent to 2.7 percent without triggering a recession

Warsh’s Policy Reversal: From Hawk to Dove

For more than a decade, Warsh positioned himself as a dedicated inflation hawk in American monetary policy with a strict interpretation of the Fed’s dual mandate of maintaining stable prices and low unemployment. His opposition to prolonged low interest rates prompted him to resign from the Fed board in February 2011, seven years before his term was set to expire, citing disagreement with policies he believed would rekindle inflation. As recently as 2021, he wrote: “If price stability is squandered, financial stability is put at risk. If financial stability is lost, the economy is imperiled, and the social contract is threatened.”

An analysis in The Economist that applied an artificial intelligence model to nearly 200 of Warsh’s speeches, television appearances, and research papers placed him firmly on the hawk end of an inflation hawk-to-dove continuum. He deviated only during severe financial crises such as the 2007–2009 global financial meltdown. That pattern held until Trump won a second term, after which Warsh reversed course, advocating interest rate cuts favored by the president. As the magazine observed, “the inflation hawk of old seems to have swapped his feathers.”

Warsh’s supporters argue that this shift reflects pragmatic flexibility rather than political accommodation. In any case, Warsh now contends that interest rate cuts will not necessarily lead to higher inflation—although many economists disagree, particularly given the upward price pressures from Trump’s tariffs. As Fed chair, he would have to persuade both financial markets and the Fed rate-setting committee that the anticipated gains from an AI-driven productivity boom and the president’s deregulation will restrain inflation.

Warsh contends that failing to cut rates now risks constraining economic growth. However, projected AI productivity gains have yet to materialize, and many economists argue that measurable improvements in worker output could be years away and modest in scale. Others contend that AI could, in fact, prove inflationary by increasing demand for energy-intensive data centers and related infrastructure.

The timing of Warsh’s policy reversal is significant. His shift from hawk to dove on interest rates coincides precisely with President Trump’s increasingly vocal interest rate views. Warsh’s accommodation raises questions about the credibility of the prospective Fed chair. Because credibility is the Fed’s most essential asset, such perceptions carry material significance.

Warsh: Fed Quantitative Easing Should Be Scrapped

Warsh argues that the Fed’s real policy error is prolonged Quantitative Easing (QE)—the large-scale purchase of government bonds and other securities by banks through the electronic creation of new money. Banks then use the funds to issue loans that stimulate the economy. While he admits that QE was justified during the financial crisis, he maintains that its continuation beyond emergencies creates a dangerous dependency as financial markets became addicted to central bank liquidity. This has allowed lawmakers to accumulate debt without consequence, resulting in higher asset inequality and a more fragile banking system.

These observations have analytical merit. Through QE, the Fed’s holdings of government bonds and securities soared from just under $1 trillion to more than $8 trillion at peak before the central bank began shrinking its holdings in 2022 through Quantitative Tightening (QT)—a process in which the Fed lets bonds mature without replacing them, thereby removing money from the system. Powell initiated QT in June 2022, shrinking the Fed’s bond holdings to approximately $6.2 trillion before the board suspended the practice in October of last year amid stress in short-term money markets.

In principle, Warsh’s framework would lead the Fed to adjust the composition of its balance sheet by retiring long-term bond holdings as they mature and replacing them with short-term Treasury bills, which typically carry lower interest rates. Over time, such an approach would move the Fed’s bond holdings toward pre-2008 levels. Implementing such a strategy under current fiscal and market conditions, however, would entail substantial risks.

A Structurally Dangerous Moment

If confirmed, Warsh’s proposed policies could thrust the nation into a structurally dangerous moment characterized by a fundamental contradiction: while the federal government pursues fiscal expansion through sustained deficit spending, its central bank seeks to constrict the money supply to control inflation. This tension would be enhanced by a bond-market rollover risk of historic proportions.

Warsh’s proposed policies could thrust the nation into a structurally dangerous moment characterized by a fundamental contradiction

Because of the composition and sheer scale of U.S. debt—expanded through years of sustained deficit spending—trillions of dollars in Treasury securities must be rolled over in the coming years. Yet rollovers will occur at a moment when interest rates are significantly higher than they were upon issuance, during the near-zero rate environment that followed the 2007–2009 financial crisis. The Fed’s benchmark interest rate fell to zero in late 2008 and remained there for seven years. Securities issued in that environment now mature under materially tighter financial conditions.

If a Warsh-led Fed were to reverse QE and accelerate balance sheet reduction, it would reduce its holdings of government bonds while the U.S. Treasury simultaneously increases the sale of new bonds to finance ongoing deficits—a classic supply-and-demand mismatch. The Treasury would be issuing new debt while the Fed—historically a major bond buyer—stepped back, removing a significant source of demand. Such a dynamic could exert upward pressure on long-term yields and further increase federal debt-servicing costs that already exceed $1 trillion annually and are on track to become the second-largest federal outlay after Social Security.

The situation would leave the Fed in a true dilemma. If it cuts interest rates to stimulate the economy under pressure from the president, it risks inflation, further undermining the Fed’s credibility. If it maintains higher rates, it risks choking growth and increasing the burden of rolling over the existing debt. Neither path is without significant danger, and the room for policy error is as thin as a reed.

If the Fed cuts interest rates to stimulate the economy under pressure from the president, it risks inflation, further undermining the Fed’s credibility

Fed Challenges Could Exceed Volcker Era

The challenges facing the incoming Fed chair could easily become steeper than those that faced Volcker, who drove interest rates above 20 percent in the early 1980s to crush double-digit inflation. Indeed, in many respects, a Warsh Fed could face more dangerous and less forgiving problems.

For one, the fiscal context is fundamentally different. Federal debt ranged from 28 to 42 percent of GDP during the Volcker era; it now exceeds 120 percent. The margin for error in monetary policy is significantly narrower: even modest shifts in interest rates carry dramatically larger fiscal consequences.

The nature of the economy has changed, too. Volcker implemented shock therapy to an economy threatened by high inflation and rising rates with a proportionally larger productive base. Warsh would have to grapple with a more financialized economy: equities, mortgages, corporate debt, and asset valuations are deeply intertwined with and acutely sensitive to monetary policy shifts. Firms and asset markets have been conditioned by over a decade of exceptionally cheap money. Any abrupt adjustment carries the risk of dislocations across financial markets in ways that Volcker never experienced.

Another unprecedented challenge Warsh faces is that globalization has eased capital controls and altered capital mobility. In the Volcker era, capital mobility was relatively benign because alternatives to dollar-denominated assets were limited. Now, emerging markets challenge the dominance of the dollar with increasingly attractive alternative investment options. A loss of confidence in U.S. monetary policy could trigger capital flight at a speed and scale that was structurally impossible in the 1980s.

No one is saying a decline of the dollar is imminent, but dollar dominance is weaker and actively contested. No comparable challenge to the dollar’s reserve status existed during the Cold War. Today, China—America’s principal strategic competitor—has announced ambitions to internationalize the renminbi, moving it toward global reserve status. Unlike the Soviet Union, economically stagnant by the 1980s, China is ascendant, versatile in dealing with the global system, and positioned to benefit from a weakening dollar. Global dollar reserve holdings have already fallen from 65 percent to 57 percent—a trend that policy missteps could accelerate.

Volcker responded to an inflationary crisis driven by oil prices in a low-debt environment, with a strong dollar and an economy supported by domestic production. Warsh, by contrast, would confront moderate-to-low inflation in a high-debt, highly financialized, and globally interconnected economy that is less dollar-dependent and far more sensitive to shifts in monetary policy. The margin for error is significantly thinner than at any comparable moment in the Fed’s modern history.

Global Effects: Dollar Credibility and Foreign Holdings

Any sign of American financial uncertainty would carry profound consequences for global financial markets. The United States has approximately $28 trillion in marketable securities held by the public, including $8.5 to $9.1 trillion held by foreign governments and institutions. The value of these holdings depends not only on market stability but also on perceptions of the Fed’s independence as a central bank capable of shielding monetary policy from political interference.

If a supply-demand imbalance in Treasury markets or a loss of confidence in Fed independence resulted in higher yields, existing foreign holders could face substantial valuation losses. More significantly, a loss of confidence could diminish foreign central banks’ appetite for dollar-denominated assets and accelerate diversification. Numerous such efforts already are underway to topple the greenback as the world’s reserve currency—a status that America uses to project power globally.

Warsh would also face something no previous Fed chair has confronted: an aggressive cryptocurrency movement seeking to integrate its products into the traditional banking system. Efforts at cryptocurrency integration into the financial architecture of the Fed introduce additional complexity, unpredictability, and potential instability.

Warsh, Fed Face Test of Backbones

The challenges awaiting Kevin Warsh are neither theoretical nor distant. If confirmed, he will inherit a Federal Reserve whose independence is under direct political pressure, whose credibility has been threatened by a significant policy reversal to accommodate presidential preferences, and whose conventional toolkit may prove insufficient for the structural pressures ahead.

The arithmetic is unforgiving: annual deficits exceeding $1.5 trillion, debt service costs exceeding $1 trillion, inflation above target, trillions in bonds requiring rollover at higher rates, and a president demanding rate cuts irrespective of prevailing economic conditions. Previous Fed chairs navigated financial crises with institutional independence largely intact and bipartisan political support for its mission. Warsh would operate under sustained executive pressure, with global markets scrutinizing whether the Fed retains the institutional backbone to resist political demands.

Global investors hold dollar-denominated assets because they are confident in the Fed’s commitment to price stability and its insulation from political interference. But that confidence, accumulated over decades, can erode rapidly. If the incoming chair accommodates White House demands for aggressive rate cuts while inflation persists and deficits expand, foreign central banks could accelerate the ongoing shift away from dollar reserves. The resulting currency pressure would magnify every other structural challenge the Fed already faces.

The convergence of fiscal fragility, bond-market rollover risk, political pressure on Fed independence, incremental reserve diversification, and a highly financialized and globally interconnected economy creates a structural environment without precedent in the Fed’s history. Whether it survives this moment with its independence intact will depend on the capacity and willingness of the incoming leadership to resist short-term political demands in favor of the long-term institutional credibility on which American financial power ultimately rests.

Whether the Fed survives with its independence intact will depend on the capacity and willingness of the incoming leadership to resist short-term political demands