European defense debates increasingly revolve around budget targets, procurement coordination, and the aspiration for “strategic autonomy”. However, these efforts skirt around a far more fundamental issue: the lack of industrial and energy depth necessary to sustain credible military power. War is not only decided by technology and manpower, but also by production lines and fuel supplies. Deterrence and defense do not just require advanced weaponry but also the capacity to maintain and replace it on a large scale.

This demands heavy industry, which in turn depends on secure, affordable, and uninterrupted energy sources. Without these foundations, European security remains a paper tiger. Nonetheless, recent initiatives show promising steps forward, such as the European Defense Fund (EDF) receiving over 400 project proposals in 2025 for over one billion euros in funding, demonstrating growing collaboration and innovation in defense capabilities.

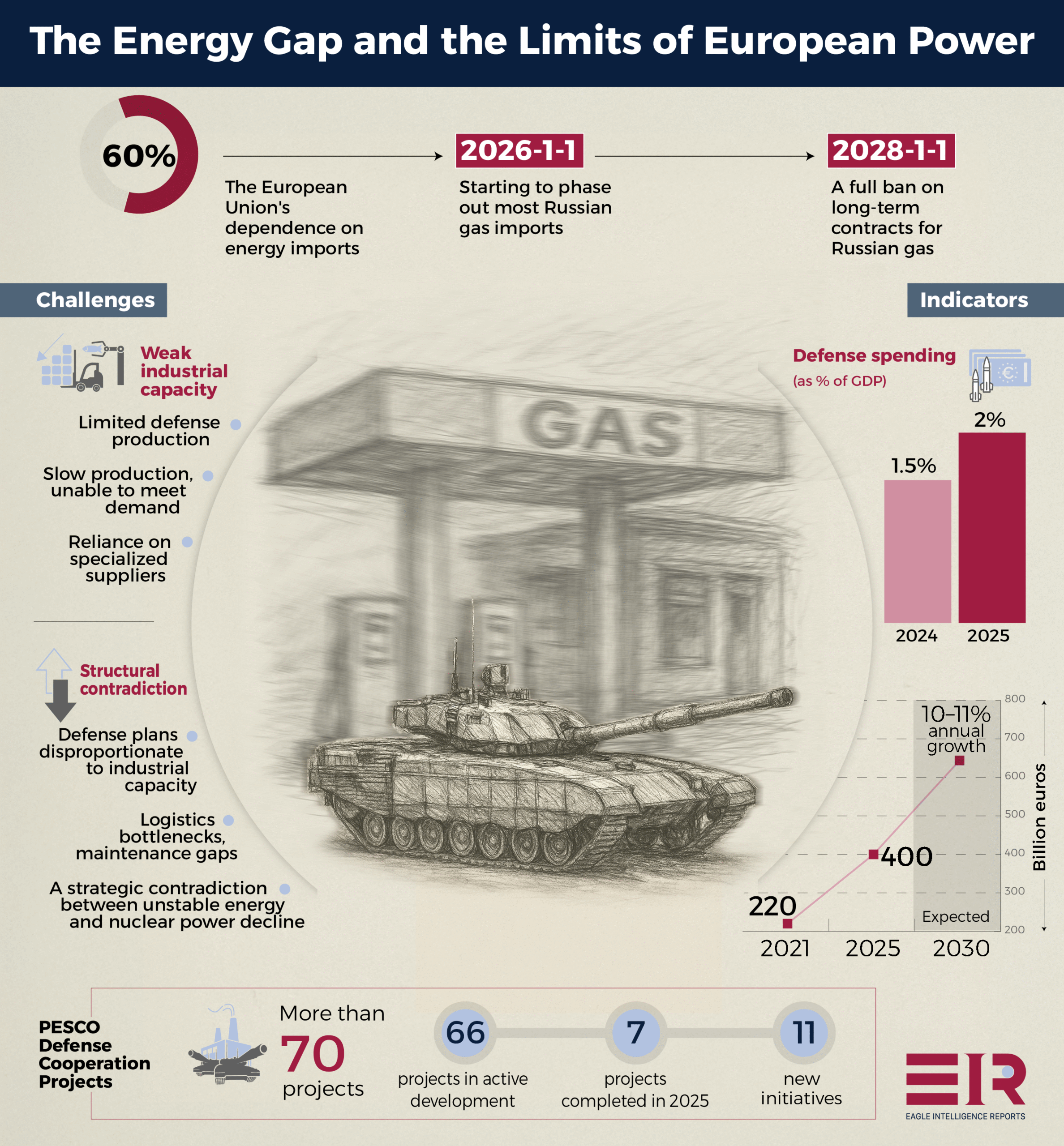

Yet a deeper look at Europe’s energy profile exposes the structural limitations that continue to undermine such efforts. The EU currently imports nearly 60 percent of its total energy demand. Its domestic production of oil and gas is marginal on the global scale, while prices remain structurally higher than in competing economies. Despite political momentum behind decarbonization, the EU’s industrial footprint continues to contract, especially in energy-intensive sectors critical to defense production.

Though defense budgets may be increasing, the continent lacks the integrated production capacity and strategic reserves to transform these budgets into scalable military capabilities. That said, EU-wide defense spending has risen to 2 percent of GDP in 2025, up from 1.5 percent the preceding year, reflecting a concrete commitment to bolstering resources amid geopolitical pressures.

Though defense budgets may be increasing, the continent lacks the integrated production capacity and strategic reserves to transform these budgets into scalable military capabilities

Additionally, the REPowerEU plan has accelerated diversification, with agreements to phase out Russian gas imports starting from January 1, 2026, for most contracts, and a full ban on long-term imports by January 1, 2028. It aims to reduce dependency through diversified LNG imports and renewable energy expansion. This industrial fragility becomes more stark when assessing Europe’s fragmented defense production base.

The Missing Industrial Base

Europe’s defense industry has notable strengths in innovation, but its industrial base remains fragmented and slow. Defense output is limited by the low scalability of production lines, overreliance on niche suppliers, and a lack of surge readiness. Ammunition factories struggle to meet Ukraine’s rising demand, and the accelerated production of armored vehicles remains sluggish.

Joint European procurement projects often stall due to diverging national preferences, insufficient standardization, and industrial protectionism. These structural inefficiencies prevent Europe from translating its economic weight into a strategic one.

On the positive side, key players like Airbus Defense and Space, Leonardo, and Rheinmetall are driving advancements, with the sector projected to grow defense spending from around 220 billion euros in 2021 to almost 400 billion euros by 2025, with further projections indicating a sustained annual growth of around 10-11 percent through 2030, fostering agility and collaboration.

The Permanent Structured Cooperation (PESCO) has also achieved milestones, with over 70 ongoing projects, including 66 in active development and 7 completed by 2025, and the sixth wave of 11 new initiatives in areas like air and missile defense and quantum technology. Still, these achievements cannot obscure a more fundamental misalignment between military planning and industrial realities.

The limitations of Europe’s defense production have become most evident in the context of Ukraine. The continent’s inability to provide sustained and timely supplies of critical materials, from artillery shells to spare parts, has exposed the gap between political commitment and industrial capability.

The Ukrainian war effort has served as an unintended audit of Europe’s military-industrial readiness: delivery timelines have often lagged behind battlefield requirements, and pledges have frequently exceeded the actual output. These operational deficits offer clear lessons about the fragility of European defense logistics, the overreliance on US stockpiles, and the fragmentation of national supply chains.

Unless addressed, these patterns will replicate under any contingency in the future, undermining both deterrence and credibility.

Moreover, industrial policy and defense strategy remain misaligned. While some member states expand defense budgets, they fail to ensure sufficient investment in industrial ecosystems needed to deliver. The result is a system unfit for sustained high-intensity warfare.

Equipment may exist on paper, but logistical bottlenecks, maintenance gaps, and personnel shortages undermine operational readiness. Without a functioning industrial hinterland, modern warfare becomes unsustainable. Europe risks becoming a military consumer, rather than a producer.

Encouragingly, the EDF’s nearly 8 billion euros budget for 2021-2027 has funded collaborative projects across 34 categories, enhancing interoperability and supporting SMEs through grants that have boosted industrial capacity in critical areas. Yet even the best-equipped factories cannot function without secure and affordable energy, the true strategic bottleneck.

Energy: The Strategic Bottleneck

Even if European defense production were more efficient, it would still be limited by the availability and reliability of energy sources. Relatively high electricity and gas prices reduce competitiveness, raise the cost of defense manufacturing, and increase the risk of supply disruptions.

Even if European defense production were more efficient, it would still be limited by the availability and reliability of energy sources

While the EU has made progress in diversifying energy imports, the system remains vulnerable to geopolitical shocks, price volatility, and infrastructure constraints. Critical defense sectors, from metallurgy to propulsion systems, depend on an uninterrupted energy supply. A factory without stable power cannot produce tanks, missiles, or aircraft.

Progress here includes the State of the Energy Union Report 2025, which highlights advancements toward 2030 climate and energy goals through reduced import dependency and tackling high energy prices through diversified sources. Solar energy’s central role in REPowerEU has further supported independence, with national diversification plans due by 2026.

The push for decarbonization, however necessary for climate objectives, poses additional constraints. Renewable energy generation remains intermittent, and battery storage is insufficient to stabilize industrial output. Some countries continue to phase out nuclear energy despite its potential as a stable power source. Plans to expand the use of hydrogen or synthetic fuel remain long-term.

This creates a strategic contradiction at the heart of European defense planning: ambitions to rearm proceed without addressing the physical prerequisites for rearmament. The result is a strategic paradox: a continent trying to rearm, while dismantling the very industrial energy base rearmament requires.

Yet, the Energy Union’s focus on security and solidarity has driven successes, such as increased renewable energy leadership and a Single Market Roadmap for integrated energy markets, which could enhance resilience for defense needs.

While national approaches vary, such as France’s emphasis on nuclear energy versus Germany’s phase-out, the EU-level framework prioritizes collective resilience over individual divergences. This brings us to the central irony of “strategic autonomy”: its rhetoric outpaces the material basis required to sustain it.

Strategic Autonomy Without Strategic Inputs

The idea of European strategic autonomy presupposes the ability to act politically, militarily, and industrially independently from the US. But this requires more than declarations such as functioning production chains, secure access to energy and raw materials, logistics infrastructure, and scalable reserves. These components are largely absent or underdeveloped.

While defense planning focuses on platforms and capabilities, it most often neglects the conditions required to sustain them in crisis or conflict. Positive developments include the European Defense Industrial Strategy (EDIS), which aims to boost cooperation in R&D, production, and procurement, ultimately reducing dependence on non-EU systems.

At the same time, the transatlantic foundation of European security is no longer assured. Political shifts in the US under the presidency of Donald Trump, coupled with growing congressional skepticism and conditions placed on critical arms deliveries, intelligence-sharing, or logistical support, could result in delays and blockades. Washington’s security guarantees can no longer be assumed as stable, timely, or unconditional.

Europe must therefore prepare for scenarios in which US military support is partial, delayed, or strategically constrained. In such cases, the gap between political ambition and operational capacity becomes existential.

Europe must therefore prepare for scenarios in which US military support is partial, delayed, or strategically constrained. In such cases, the gap between political ambition and operational capacity becomes existential

Strategic autonomy, apart from sovereignty, requires systemic resilience in the absence of guaranteed external support. The limitations revealed by delayed and fragmented European support for Ukraine serve as a live stress test of Europe’s strategic autonomy.

If Europe cannot sustain one war at its periphery without US logistical, industrial, and political cover, it cannot credibly claim autonomy in any future crisis.

Initiatives like PESCO’s military mobility project, involving non-EU partners like Canada and Norway, exemplify initial progress toward improving infrastructure through cross-border coordination, but remain far from achieving operational self-sufficiency.

The Operational Reality

Nevertheless, military capabilities are measured by operational efficiency, not political declarations. European NATO members collectively possess a vast arsenal of military equipment, but operational readiness varies dramatically. Many systems are obsolete, mothballed, or incompatible.

European land forces lack sufficient engineering units, electronic warfare capabilities, and long-range precision munitions. Air defense coverage is sparse, especially in Eastern Europe, and strategic airlifts remain dependent on US or civilian capacity.

Cyber capabilities are uneven, and supply chain security for defense production is insufficient. However, the EU’s Defense Readiness 2030 Roadmap outlines ambitions to address these, with tangible progress in joint capabilities.

And the gap between stated capability and real-world performance grows more dangerously in the face of adversaries that learn and adapt under fire. Exercises remain limited in scale and realism. Large-scale joint maneuvers often rely on simulation rather than actual troop deployments.

The ability to coordinate corps-level operations across multiple national units is still aspirational. Crucial enablers, such as logistics, reconnaissance, and command and control, are either lacking or reliant on US assets. In a major war scenario, these shortcomings would become liabilities within days.

Meanwhile, Russia has demonstrated its ability to mobilize large forces, sustain production volumes under sanctions, and exploit Western hesitation. Its war economy functions through a combination of fiscal-military mechanisms such as OFZ bond financing (federal loan bonds; Russia’s primary government securities), oil-funded budget loops, and industrial patronage networks that ensure priority allocation to defense enterprises.

Despite severe losses, the Kremlin has preserved core production capacities and adapted supply chains to circumvent sanctions, relying increasingly on grey imports and parallel trade with China, Turkey, and Central Asia.

China has pursued long-term investments in military-industrial expansion, dual-use technology dominance, and state-led innovation, aiming to secure strategic parity over decades.

In contrast, Europe faces a critical triangle of logistical, industrial, and institutional fragility, which undermines its capacity to respond autonomously to protracted or high-intensity conflict.

Rebuilding the Foundations

In the coming years, Europe has to address its structural gaps. It needs a coherent defense-industrial policy that focuses on scale, readiness, and resilience. This means maintaining strategic production lines, securing critical supply chains, and investing in industrial redundancy.

In the coming years, Europe has to address its structural gaps. It needs a coherent defense-industrial policy that focuses on scale, readiness, and resilience

Additionally, its energy policy must be reformed to integrate security imperatives, such as stable baseload generation, support for defense-critical sectors, and a realistic approach to the transition timeline.

Finally, Europe must invest in the coordination infrastructure needed to manage complex joint operations: command centers, logistics hubs, and interoperable communication systems. Successful examples include PESCO’s progress report for 2025, which highlights deliverables from the first phase (2017-2025) and sets the stage for future advancements.

None of this can be achieved overnight. But the window for adjustment is narrowing. If Europe fails to act, it will remain strategically dependent and militarily vulnerable. Rhetoric will not deter aggression; industrial power, embedded in stable systems and governed by coherent strategy, will.

Europe’s security deficit is not simply a failure of political will; it reflects the deeper erosion of the industrial and energy systems that underpin credible defense. Without addressing these structural weaknesses, strategic autonomy remains not only symbolic but strategically misleading.

The lesson of warfare is unambiguous: wars are won not just on the battlefield, but in the factory, the power grid, and the logistics chain. Europe must relearn this lesson or remain an exposed periphery in a multipolar confrontation.

While recent measures, including increased defense spending, PESCO advancements, and energy diversification, are steps in the right direction, they remain insufficient. Without a structural reset of Europe’s industrial and energy base, the vision of strategic autonomy will remain performative. The next crisis will expose whether Europe can truly rearm or merely rebrand.